Most of my introductory remarks about Japan (JP) to follow are based on two EIA reports: a country analysis report on Japan, and, a report on the East China Sea.

It might seem odd to include JP, a relatively small country, in a nine-region global analysis of global petroleum consumption trends. However JP’s petroleum consumption as a country is third only to the USA and China Japan

What Japan Okinawa , in an island chain called Daioyu/Senkaku (Chinese/Japanese name). As the dual naming implies, there is an ownership dispute for these islands between China and Japan

The EIA estimates that the East China Sea has between 0.06 and 0.10 bbs of oil in proven and probable reserves, but, China China

In view of JP’s lack of domestic oil, it should be no surprise that JP’s present consumption rate is almost totally reliant upon the continued importation of oil from one or more of the other eight regions featured in this series.

Let’s take a look at what regions Japan imports its oil from, and, what the import trends from those regions to JP look like.

Japan’s production, consumption and net export trends: an ELM analysis

My usual source of data, the BP Statistical Review, reports JP’s petroleum consumption rate, but, does not report information about JP’s domestic production rate—I suppose because the number is too small to meet the Review’s reporting criterion. Therefore, the data for JP’s production was from the EIA’s International Energy Statistics Division, corresponding to the EIA’s “total oil supply,” which reports back to 1980.

Figure 34 presents the reported production, consumption and calculated net exports rates (dark blue, bright red and dark green open circles respectively) and the corresponding nonlinear least squares analysis (NLLS) logistic equation best-fit curves (solid lines with the same respective colors). To calculate net exports before 1980 I am assuming that JP's production was equal to zero. The solid green line before 1980 is based on a back-extrapolation of the logistic equation best-fit to the 1980-2011 EIA data set (see Figure 34a).

At the vertical scale used in Figure 34, you can barely see JP’s miniscule production rate, so I reproduced the production data and the NLLS best fit in Figure 34a, below:

The best fit parameters of Qo, Q∞ and the rate constant "a" are summarized in Table 8 below:

Table 8 summary of best fit parameter for production and consumption data for JP

| |||

Qo (bbs)

|

Q∞ (bbs)

|

a (yr-1)

| |

Production 1980-2011

|

0.16

|

2.3

|

0.084

|

Consumption 1965-1982

|

3.7

|

41

|

0.19

|

Consumption 1983-2011

|

25

|

106

|

0.077

|

As illustrated in Figure 34a, JP production rate has increased substantially since 1980, although there are signs that the growth in the production rate has stalled-out and in for a decline, as implied by the NLLS fit.

It might seem curious that the production rate in the last several years, about 0.05 bby, actually exceeds the EIA’s estimate of total reserves, of about 0.044 bbs. The discrepancy is explained by the fact that, by far, the bulk of JP’s production is from “refining gains,” from the country's domestic petroleum refining sector. For instance, according to the EIA Japan country analysis report, in 2011 of its total 130,000 b/d production rate, JP only produced 5000 b/d of crude oil. In other words, less than 4% of JP’s production corresponds to actual crude oil being produced domestically.

Similar to that discussed for Europe in Part 7 of this series (and discussed in Part 10 of my early Trade Movements series) it seems that JP has found a way to profit by importing crude oil, refining the oil domestically, and then re-exporting some of the refined products to other regions. For instance, according to the EIA (citing the Oil & Gas Journal), JP has a refining capacity of 1.7 bby (4.7 mbd) which is second only to China China and the remain Asia-Pacific regain, similar to the way Europe exports to North America and Africa .

Figure 34 shows that JP’s consumption rate has clearly been in decline since the late 1990s. It looks like the consumption rate peaked in 1996, at about 2.1 bby, and after about 5 years of a shallow decline, the consumption rate started to decline more steeply through the 2000s from 1.97 in 2001 to about 1.61 bby in 2011. This corresponds to an 18% decline in the last 10 years, or, a 24% decline in the last 15 years from the peak in 1996. In other words, JP has been experiencing annual declines in its petroleum consumption rate in the range of 1.6-1.8 %/yr for last decade-and-a-half.

If you squint hard at the red circles in Figure 34, you will see a slight up-tick in consumption in 2011 compared to 2010. This is probably reflecting the effects of the tsunami and subsequent Fukushima Daiichi nuclear plant shutdown in March 2011, and then a country-wide shut down of nuclear power plants. The slight up-tick in petroleum consumption reflects increased electricity generation from petroleum-fueled generators. It was only in July 2012 that the first nuclear plants began to reopen, so the trend of increasing petroleum consumption, or at least a less steep decline in petroleum consumption, might continue into 2012 and beyond.

The order-of-magnitude greater consumption rate (red line) compared to production (blue line) is also readily apparent in Figure 34, illustrating how JP is a huge net importer of petroleum (green line). Given JP’s low domestic production rate, it is not surprising to see that JP’s year of peak imports was in 1996, the same year as JP’s peak consumption rate. Still, in 2011, at +1.52 bby in net imports, 94% percent of Japan

Predicting Petroleum Export Rates from JP to other Regions

Figure 35 shows the relationship between petroleum production rates and export rates for JP, as already worked out in my previous study from a few months ago. This is the same as Figure 4 in Part 2 of “Relationship between Petroleum Exports and Production.”

The proportion of JP’s total exports, expressed as a percentage of production (black Xs, rhs scale), is increasing (r2=0.78). This linear regression line is likely reflecting the combination of flatting production rates, i.e., flatting refining gains, and increasing refined product exports. That these percentages are greater than 100% of domestic production is perhaps not so surprising now that we see how JP has been functioning as a middle-man for the regions that export crude oil (i.e., the Middle East) and the remaining Asia-Pacific countries (rAP, blood red line) and China (CH, pink line) who are import JP’s refined products.

For instance, as illustrated in Figure 35, in 2011, 77% and 15% of JP’s exports went to rAP and CH, respectively, with the remainder going to NA and EU. In 2011, according to the BP Statistical Review, JP’s total exports to other regions amounted to 0.11 bby (290,000 bpd) of products and 0.00022 bby (1,000 bpd) of crude oil—I wonder where that 1000 barrels of crude got exported to, and, why export it, given JP’s large refining capacity. In contrast, JP’s total imports were 1.3 bby of crude oil (3,560,0000 bpd) and 0.34 bby (930,000 bpd) of petroleum products.

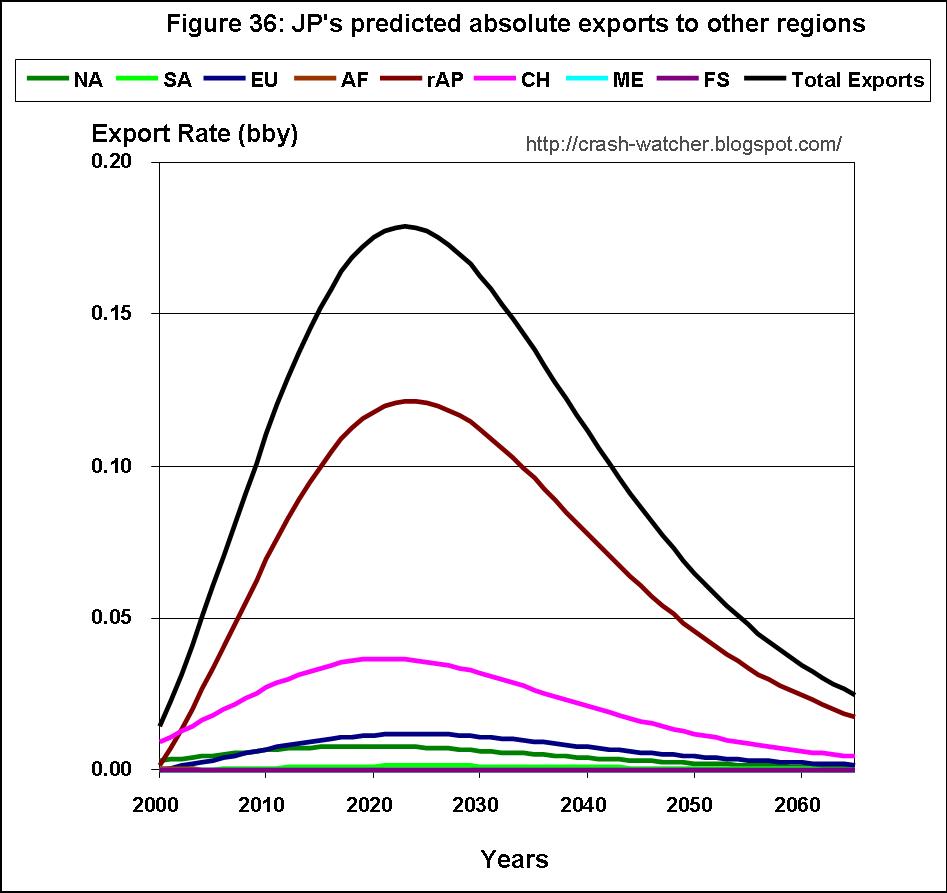

Figure 36 shows the predicted absolute regional exports from JP to the other regions, based upon the combination of the production rate trends shown in Figure 34a and the export trend lines shown in Figure 35.

According to this prediction scenario, JP’s exports will top out at about 0.18 bby in 2023, and most of those exports will go to rAP and CH in a ratio of about 3.4:1. The reason for the downturn after 2023 is due to the predicted decline in domestic production in Figure 34a (again for JP, mostly reflecting declining refining gains as imports decline). Declining production overcomes the upward export trend shown in Figure 35. Of course, the absolute amounts of these exports are very small compared to the exports to and from any of the other eight regions considered in this series, although they may be still be important to some countries in the rAP region that gets most of JP’s exports: Australia, New Zealand, Singapore and China.

Predicting Petroleum Import Rates to JP from other Regions

Figure 37 shows the sum (black line), and individual import contributions, predicted for each of the other eight regions, to JP.

In part Part 7 of this series, I showed a pretty grim picture for Europe ’s future imports. But, the import picture for Japan looks even grimmer than Europe ’s, mainly because JP is so heavily dependent on the ME for its imports.

As shown in Part 2 of this series, not only is ME’s production toping out and likely about to decline, but the proportion of ME’s production being exported is strongly trending downwards. Moreover, the situation is even worse for JP, because ME’s downward trend of exports to JP is even steeper than its overall downwards export trend. This is due to ME’s increasing proportion of exports going to rAP and CH, to the detriment of NA, EU and JP.

However, of the three regions NA, EU and JP, it is JP by far that is most dependent on receiving imports from the ME. For instance, from the prediction curves Figure 37, in 2011 about 79% of JP’s petroleum imports corresponding to about 1.2 bby, came from ME and about 10% came from rAP. Projecting out 10 years to 2022, ME is predicted to still provides 76% of JP imports, but the absolute amount will be only about 0.6 bby, a 50% decrease from 2011. It is JP's high dependence on ME's oil, as I said in an earlier post would cause JP to be especially devastated by a sudden disruption in oil flow from the ME (see: If the Strait of Hormuz Closed, Which Importing Region Would Suffer the Greatest Loss?).

The only slightly bright-spot for JP’s future import picture is that imports from FS and NA are predicted to increase (Figure 37, purple and dark green lines, respectively).

Unfortunately, the rate of increasing imports from FS and NA barely offsets the rate of declining imports from rAP, let alone from the ME. And, because FS’s production rate is predicted to being peaking about now, absolute imports from this source are likely to go down after about 2017. Projecting out even farther to 2030, if these trend continue, JP's total imports will have declined to about 21% of its imports in 2011.

Since JP has substantially no domestic petroleum production and minor petroleum exports, it is no surprise to see that my PIE analysis predicts a petroleum consumption rate curve that essentially mirrors the predicted total import curve in Figure 37 (black line).

I applied my normalization to JP in the same manner as done for NA, SA, AF and EU. For JP, the average calculated consumption rate, based on the summation of production plus imports minus exports for the 2001-2011 time range, was 0.038 ± 0.036 bby lower than the reported consumption rate for JP as reported in the BP review. Therefore my normalization for JP consisted of adding 0.038 bby to the predicted future consumption rate and adjusting total net exports downwards by this same amount. And, like the other regions, I did not attempt to distribute this correction proportionally among the individual absolute exports and absolute import to and from each of the other regions.

Figure 38 shows the production, consumption and net export data, and corresponding best fit curves, the later two now shown as dashed lines. Added is the predicted net export (light green solid line representing total absolute exports minus total absolute imports with the -.038 bby correction) and consumption (blood red solid line) rate prediction curves, based on my PIE analysis (exports minus imports with the 0.038 bby correction).

The results presented in Figure 38 suggest that, if JP’s production rate follows the decline trend predicted by the logistic equation best fit (solid blue line), and JP’s export and import rates continue along the trend lines shown in Figures 36 and 37, respectively, then the predicted total net export rate curve (solid light green line) is going to continue declining, until about 2041, after which, net export become more negative as imports from NA increase.

JP’s predicted consumption rate (blood red line) almost exactly mirrors the net export curve, which almost reaches zero in 2041, before going up again slight due to imports from NA. The predicted rate of decline in consumption is even steeper than the already steep decline predicted by the logistic curve fit to the consumption rate data (dash line in Figure 38 and solid red in Figure 34). That is an annual decline rate that’s even steeper than the decline rate of -1.6-1.8 %/yr over the last 10 to 15 years. For instance, the predicted consumption rate is 1.42 bby in 2012 and 0.68 bby in 2022—a 52 % decrease over 10 years or about -5.2 %/y. That’s much steeper than the consumption rate declines of -2.2 %/y predicted for NA and -3.2 %/yr for EU, earlier in this series.

Final thoughts

There is a slow-motion disaster occurring in Japan

According to the EIA country analysis report in 2010, nuclear power provided 13% of Japan Japan Japan

Total energy decline rates of -2.3 %/y to -0.8 %/y would mean that it would take about 6 to 16 years to have a total energy consumption decline that is the petroleum energy equivalent of shutting down all of Japan Japan

However, if the declining export trend to JP continues, then, in less than 30 years (about 2041), Japan

I think that the effects of having no petroleum to consume go well beyond the loss in 44% of total energy consumption provided by oil, because of oil’s vital role in transportation. That is, to what extent could the infrastructure to support that other 56% of energy sources could be sustained in the face of little to no oil?

Given these trends, I find it very hard to imagine how Japan’s economy (e.g., as measured by GDP or GDP per capita) would have any chance of remaining at present levels in the face of -5 %/yr declines in petroleum consumption. Rather, for the next 10-15 years Japan

If the East China Sea really did have oil reserves equal to +10 years of Japan ’s present consumption rate, and, Japan could acquire that oil through diplomacy or war against China

Absent such an event, however, within the next 30 years as oil exports from the Middle East end, Japan

------------------------------------------

Next time, I will cover one of the last two regions in my 9-region analysis: China

No comments:

Post a Comment

Your comments, questions and suggestions are welcome! However, comments with cursing or ad hominem attacks will be removed.