"Globally, we find more (oil) all the time, but we haven't actually found as much as we've used in a given year since 1985," said Maj. John Sheahan, another member of the research team.

"From the long (term) view, it's guaranteed that something else will take over (as an energy source), we just don't know what or when. Nobody has yet come up with the solution (so) that we can (continue to) do the things we do now and have done for decades.

"So it is possible that the timeline is against us."

Yes Major, I do believe that the time line is against you, and you probably know this for a fact. What is not guaranteed is that there will ever be a replacement which has the energy density and transportability of petroleum. This news story is yet another example of what we have being starting to see with increased frequency: military and government study groups and companies all talk openly about the problems that lay directly ahead, while the public and politicians remain largely asleep—or at least silent.

Part 2 and part 3 of this series presented a regional analysis of global petroleum production and consumption trends for the Middle East (ME), Former Soviet Union (FS), Africa (AF), South America (SA), Asia-Pacific (AP), Europe (EU) and North America (NA). Part 4 used this data to predict how the global petroleum export pool will likely decline to zero in about 2030-2035. Part 5 used the data to predict what petroleum consumption will look like for each of these regions as global net-export pool declines to zero.

Here in part 6, I analyze the same data to predict peak oil and total recoverable petroleum (Q∞; sometimes referred to as URR, ultimate recoverable reserves) for these seven regions, and for the world.

I also briefly compare my predictions to predictions made by others, and, present a fantasy consumption scenario for North America .

A simple analysis of global petroleum production

Figure 19 shows the reported global petroleum production and consumption data from the BP statistic review and the best fits of single Hubbert Equations to these data sets:

The best fit parameters from these fits are summarized in Table 9 below:

Table 9: summary of best fit parameter for world production and consumption | |||

Qo (bbs) | Q∞ (bbs) | a (yr-1) | |

Production 1965-2009 | 611 | 4135 | 0.030 |

Consumption 1965-2009 | 528 | 4073 | 0.032 |

If properly accounted for, global annual consumption must equal global annual production. But, as I pointed out in Part 5, for the past 30 years, the BP data base has systematically reported annual world production rates that are lower than the annual consumption rate, and before that, the opposite systematic difference existed (reported production always greater than consumption). If you look at Figure 19 carefully, comparing the open red and blue circles for each year, you can see this trend, which as I mentioned before is not explained by BP. The systematic difference explains why the best fit parameters are slightly different for production and consumption data.

The best fits to both data sets, however, are quite close, and basically tell the same story: world production rates are increasing at about 3 percent per year (“a” = 0.03 yr-1), the total recoverable petroleum (Q∞) equals about 4 trillion barrels and the peak production rate of 31-32 billion barrels per year (bbs/yr) will not occur until 2023. These broad curves suggest that global production could plateau at or slightly above present levels for another 20 years.

This suggestion of a broad, slowly declining production curve is akin to what I have referred to in past as the rosy peak oil scenario. The rosy peak oil view admits that oil production will peak and decline, but the decline will play out over decades. This implies that there will be a good amount of time (e.g., decades) to adapt our transportation network, food production infra-structure, manufacturing sector, etc... to a world with gradually declining petroleum resources.

My 7-region analysis and its composite sum suggests a quite a different scenario than this simple analysis.

Seven region analysis of global petroleum production trends

As explained previously in parts 1-3, because the production curves for the seven regions (shown in Figures 1-7, in part 2 and part 3) are not described very well by a single logistic curve, I fit separate multiple Hubbert equations to different time spans of the production data for each of the seven regions.

If the separate Hubbert Equations were completely separated in time (due to having been fit to well-separated peaks in reported production at different times) then the best-fit Q∞ values from these separate fit would add up to the total recoverable oil. But, because this is not the case, and there is substantial peak overlap, the best-fit Q∞ values from these separate fits do not equal total recoverable oil for the region.

However, I can use the best fit parameters from these separate fits to generate a single simulated production curve, and then integrate total area under the simulated curve to calculate an overall Q∞ for the region.

I used the values of the Hubbert Equation parameters, Qo, Q∞ and "a," obtained from my best-fits to the production data, to produce such a simulated curve with the simulated curves interpolated far into the past and future. Then I added up (i.e., digitally integrated) the annual dP/dt values to estimate the value of Q∞, the total recoverable oil for that region. To perform the digital integration, I interpolated out to dP/dt values of 0.1 bbs/yr in future and past time directions, and summed the cumulative dP/dt values in between these two 0.1 bbs/yr values (somewhat variable from region to region, but generally about the 1950s to 2050; NA was an exception: 1938-2143).

Table 10 shows the estimates of Q∞ for each of the seven regions using this method. Table 10 also presents my estimate of how much petroleum was used up to 2010 (i.e., Q2010, the area under the curve up to 2010) and what percentage this is of the total area (i.e., what percentage has been produced, or the percentage of depletion, by 2010).

Table 10: Summaries of best fit parameter for regional total recoverable petroleum | |||

Q∞ (bbs) | Q2010 (bbs) | % depletion 2010 | |

517 | 325 | 63 | |

470 | 254 | 55 | |

Former | 270 | 180 | 67 |

Asia-Pacific | 186 | 95 | 51 |

168 | 100 | 59 | |

137 | 117 | 85 | |

75 | 65 | 87 | |

I presented the seven regions in Table 10 in order of decreasing Q∞. All seven of the regions by 2010, have less than 50% of their total recoverable petroleum remaining and some have produced substantially more than half. EU and AF, for instance, have already used more that 85% of their recoverable petroleum. For EU, this is likely because the North Sea oil reserves have been on the decline-side of the production curve for several years. For AF, this is because of the recent sharp increase in production rates and the subsequent sharp transition to the decline-side of the production curve at the same rate. This is why in part 6, I suggested that AF and EU will be in serious trouble when the global export pool hits zero in 2030-35.

Peak oil aficionados will understand that “peak oil” refers to the all time maximum in the production rate (dP/dt). “Peak oil” is often incorrectly defined as the point where half the oil has been pumped out of the ground, or, “produced.” The time when half of the recoverable oil has been produced (i.e., ½ Q∞), and the time of maximum production rate (“peak oil”), only coincide exactly when the time course in production rate follows a single Hubbert Equation. That is, “peak oil” and ½ Q∞ only coincide in time when a logistic curve accurately describes the entire time course of production of the well for whatever is area is being considered—the well, the group of wells, or all the wells in a country or region, or the world. This rarely, if ever happens in practice. When this doesn’t happen, “peak oil” and ½ Q∞ do not necessarily occur in the same year.

The best fits of Hubbert Equations to the production data for the seven regions, and the digital integration of the extrapolated best fit simulated curves for each region, allowed me to estimate both the year of peak production rate (i.e., the year of “peak oil”) and the year of ½ Q∞, both of which are summarized in Table 11 below.

Table 11: Summaries of regional years of Peak Oil and 50% depletion | ||

Peak Oil | ½ Q∞ | |

2007 | 2002-2003 | |

2005 | 1985 | |

Former | 2012 | 1999-200 |

Asia-Pacific | 2006 | 2009-2010 |

2008 | 2003-2004 | |

2007 | 1994-1995 | |

1999 | 1997 | |

Global petroleum production trends from the cumulative sum of the 7-region analysis

Figure 20 shows the predicted global production rate (the blue curve) as the composite sum of the simulated curves from the best fits of the Hubbert Equations to the production rate data for each of the seven regions. For reference, I also present the reported global production data (open blue circles), which is the sum of the reported production data for the seven regions.

The composite sum of the prediction curves for the seven regions is in very good agreement with the reported global production rates from 1965-2009.

Even though the 7-region sum is the sum of separate best fits to seven different production curves, the composite curve shows a nearly linear decline-side slope from 2010 to 2030 of about 0.78 bbs/yr per year. That is, the total global production rate is declining by 0.78 bbs/yr (~2 mbd) every year for 20 years, before the decline starts to tail off to a lower rate.

Next, I estimated the global total recoverable petroleum, or, ultimately recoverable reserve (Q∞) by taking the sum of the regional Q∞ values reported in Table 9. The total amount of global petroleum recovered up to 2010 (Q2010) was estimated from the composite curve. The composite curve for the seven regions was also used to estimate the year of global peak oil and the year of 50% depletion. The results are summarized in Table 12.

Table 12: Global production parameters from the sum of the 7-region analysis | ||||

Q∞ | Q2010 | % depletion 2010 | Peak Oil | ½ Q∞ |

1823 bbs | 1136 bbs | 62 | 2007 | 2002 |

Figure 21 compares the 7-region composite curve (solid blue line), the single Hubbert Equation best-fit (dashed blue line) and the reported total world production data (open circles). For reference, I also show the net global export rate curve, which was discussed in Part 4 (see Figure 8).

The predicted production rate curve based on the 7-region composite curve clearly fits the reported data (open circles) much better than the single Hubbert Equation best fit does. This makes sense to me because the composite curve actually represents the analysis of seven times more data (i.e., fits of multiple Hubbert Equations to each of the 7 region’s reported data) than the single data set (i.e., fitting one Hubbert Equation to the global reported production). For this reason, I believe that the estimated parameters, Q∞, 50% depletion, peak oil and ½ Q∞ should be much more accurate than the analogous parameters from the simple Hubbert equation analysis of global petroleum production.

If the curve from the composite sum of the 7-regions is the more accurate of the two predictions, then the future does not look like a rosy peak oil scenario. Instead of a 20-year period with a plateau in production at or slightly above present rates, we are on the brink of going down the steepest part of the production decline curve. My composite curve predicts that total world production will go down every year by 0.78 bbs or about 2 mbd, for the next 20 years. And, instead of living in a world with 4 trillion barrels of total recoverable oil, of which we have only extracted 1.1 trillion barrels, we live in a world with 1.8 barrels, of which we have already extracted 1.1 trillion barrels, leaving only 0.7 trillion barrels left. Instead reaching a production maximum in about 2023, we have already past peak oil three years ago. In a world whose economy is driven by, and whose people are fed with, petroleum, the decline in liquid energy wealth is directly ahead, not a decade or so away.

Despite how bad this sounds, I think that it is even worse for the importing regions of the world, because over this same 20 year period, global net exports will decline from about 13 bbs/yr (35 mbd) to zero. The importing regions will be facing their own declining production, plus, the declining pool of exportable oil, at the same time.

The assumption of symmetry

In contrast to a widely discussed theory that world oil production will soon reach a peak and go into sharp decline, a new analysis of the subject by CERA finds that the remaining global oil resource base is actually 3.74 trillion barrels -- three times as large as the 1.2 trillion barrels estimated by the theory’s proponents -- and that the “peak oil” argument is based on faulty analysis which could, if accepted, distort critical policy and investment decisions and cloud the debate over the energy future. ....

Global production will eventually follow an “undulating plateau” for one or more decades before declining slowly. The global production profile will not be a simple logistic or bell curve postulated by geologist M. King Hubbert, but it will be asymmetrical – with the slope of decline more gradual and not mirroring the rapid rate of increase -- and strongly skewed past the geometric peak. It will be an undulating plateau that may well last for decades.

I don’t know how CERA came up with their prediction, but it sounds a lot like my simple single Hubbert Equation analysis described above—a Q∞ of ~4 trillion and one or more decades of undulating plateau. I am not going to pay the several hundred dollars they charge for their report, and, I’m not even sure that report would describe their methods. For the sake of their subscribers, I hope that CERA did do something more elaborate than my simple analysis! But whatever analsysi they did, they arrive at about the same result as my simple single Hubbert Equation analysis, which I think is far less accurate than my seven-region analysis.

I am sympathetic , however, to the possibility that global oil production could follow an asymmetrical decline curve, and not the simple logistic curve as assumed by the Hubbert Equation.

For instance, as I have shown previously, there is good evidence that the production growh and decline side curves for the USA

Because the USA

In the present study, however, many of the other regions (ME, AF, AP, FS, SA) are just approaching, or just at, peak production, and therefore there isn’t enough data on the decline side of the production curve to assess the possibility of asymmetries between the growth-side and decline-side of the production curve.

I suppose that I could just assume a certain fac and fcq value for the other regions (ME, SA, AP, AF), but in my opinion, there is no factual basis to suggest that new recovery methods or newly discovered oil, will continue to occur global at the same rate as it did over the past 50 years for the USA. That is, it is not a given that all regions will have asymmetries similar to that of NA. For instance, consider the last 20 years of data for EU, which includes growth and the decline sides of its production curve. The growth and decline sides of the production rate looks very symmetric, and, consequently the best-fit of the Hubbert Equation to this range of data looks very tight (see e.g., Figure 4, Part 3, comparing dark blue curve and blue open circles).

Additionally, there is evidence that the decline side for the other regions of the world may not be long and drawn out like it has been for the USA, and instead more like EU.

For instance, the newer off-shore oil wells appear to be depleting at a much fast rate than older on-land wells (see e.g., Giant oil field decline rates and their influence on world oil production). Perhaps this explains why EU’s production curve, which is dominated by North Sea off-shore oil production, has such a sharp decline-side.

For instance, the rate of discovering new wells is much lower than the rate of discovery in the past. (see e.g., Figure 1 Conventional Crude Oil Discovery and Production Rates to 2005 with Projections to 2030, from Colin J. Campbell in The Oil Age: World Oil Production 1859–1950, reproduced in: Crude Oil Supply - The Oil Age: World Oil Production 1859–1950).

It follows, therefore that modern methods of recovering of oil from off-shore wells may not lead to a drawn out decline side, and, the potential development of new petroleum resources that would prolong the decline, are greatly reduced because the recent past discovery rate has declined substantially.

Perhaps it is CERA’s hoped for asymmetric shallow decline-side curve, that is the “faulty analysis” and one that is designed to distort “critical policy and investment decisions” and “cloud the debate” over the energy future. I think that we will find out soon enough. I'm hoping (but not expecting) that I an wrong, and, that there will be asymmetries on the decline side.

Therefore, in the absence of stronger evidence of growth-side and decline-side asymmetries in the production curve, I have chosen, or the data leaves me no choice but, to model the production data with multiple Hubbert Equations, with their inherent symmetry assumptions.

Comparison to other predictions

Ultimately recoverable conventional oil resources, which include initial proven and probable reserves from discovered fields, reserves growth and oil that has yet to be found, are estimated at 3.5 trillion barrels. Only a third of this total, or 1.1 trillion barrels, has been produced up to now.

Executive Summary IEA, World Energy Outlook 2008

The global resource base is 4.82 trillion barrels and likely to grow. CERA’s analysis of global reserves and resources includes both conventional and unconventional oils as well as estimates of both field upgrade potential and yet to find. With some 1.08 trillion barrels of cumulative production to date, 3.74 trillion barrels remain, which is three times larger than the typical peakist estimate of 1.2 trillion.

Why the “Peak Oil” Theory Falls Down CERA 2006

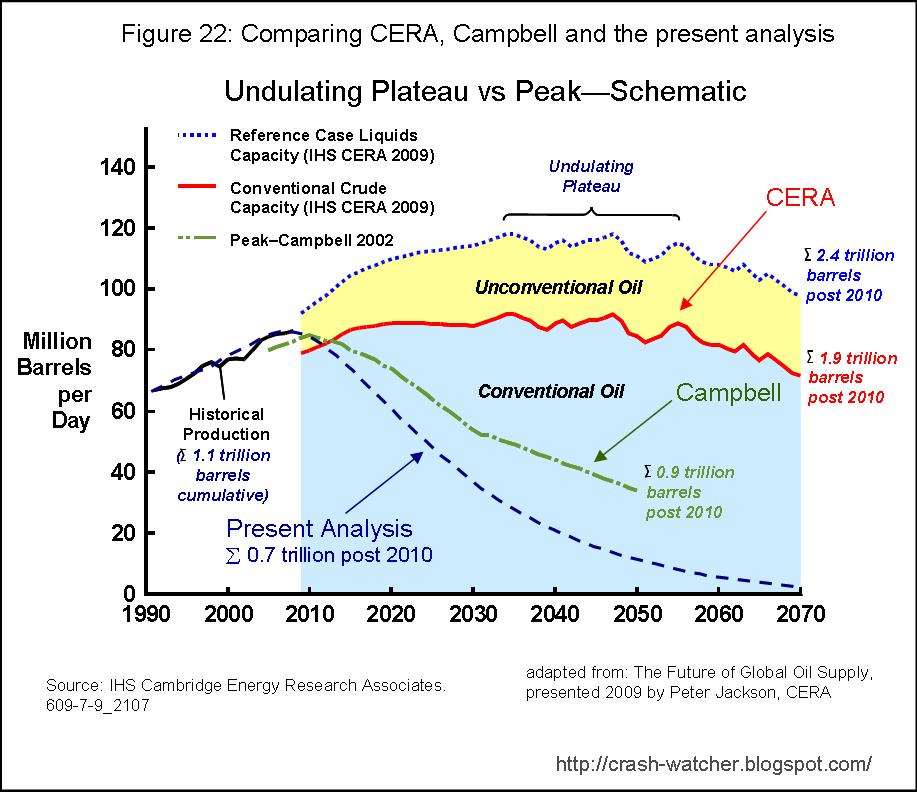

Figure 22 below is reproduced from a 2009 CERA presentation by Peter Jackson (The Future of Global Oil Supply) compared the CERA and Campbell’s predictions of future production trends.

To this, I have added the predicted global production from the present analysis (i.e., cumulative 7-region analysis to predict global production—Figure 20 above).

Also illustrated below in Figure 23, is the IEA’s estimates of future production, reproduced from the IEA’s World Energy Outlook 2008, which are about the same as CERA’s.

CERA, the IEA and my present analysis are all in agreement in that the total amount of petroleum produced to data equals about 1.1 trillion barrels.

However, my present prediction of Q¥ equal to 1.8 trillion barrels is much more pessimistic than CERA’s and the IEA’s prediction that Q¥ equals about 4-5 trillion. Again, CERA’s and the IEA’s predictions look similar to my single Hubbert Equation analysis presented above.

My prediction is even a bit more pessimistic than Campbell’s 2002 prediction, in that I am estimating that only 0.7 trillion barrels of recoverable oil remains in 2010, whereas Campbell’s 2002 prediction estimates 0.9 trillion barrels. I am not aware of a more recent prediction made by Campbell, that considers at least some of the last 8-9 year’s worth of data, but it would be interesting to see how this would have changed Campbell

Interlude: A North American Consumption Fantasy

(Except for portions of the first paragraph to follow, I do not believe that the scenario laid out below is very likely to occur—but I have set this scenario up for illustrative purposes, as will soon become apparent.)

A new President of the USA USA

Unfortunately, the President-elect is a complete math moron and sociopath, and, he is surrounded by advisors that are also morons and sociopaths. In his first state-of-the-union address, the President makes the following announcement:

I will never, never, never, allow the people of America America USA

Being a moron, the new President believes that the only way to prevent Americans from freezing in the dark, and to continue the American dream, is to ensure that per capita oil consumption continues at its long-standing rate of 21 barrels per person per year (b/py).

Back to the new President’s speech:

Therefore I am announcing here today a new free energy doctrine (FED). To fulfill the mandates of the FED, I am immediately declaring war on all countries of the world outside of North America . From this point forward, the rest of the world outside of North America must reduce its oil consumption to the equivalent of 2 b/py and also give the remainder of their oil resources to the USA , for free, so that we, the great people of America

Factor X is a very special weapon that only kills humans, doesn’t do damage to the petroleum infrastructure, and, then dissipates immediately. Also (to make this fantasy work), the US military has been training an unlimited number of soldiers to be petroleum engineers and technicians, who can, after killing everyone, drop in and operate all of petroleum production and refining facilities in a country so that its production rate can continue unabated. Fortunately for Mexicans and Canadians, applying Factor X in these countries would cause too much collateral damage in the USA USA North America and all elections are suspended indefinitely in this state of emergency.

The few protests against this unilateral action are quelled when the President announces a new stimulus bill that includes supplying every household in America

Okay, enough of that, Figure 24 shows the consequences of such a scenario:

(5-9-11: revised figure 24 and narrative to account for the changes in NA data in Figure 18 from Part 5; the overall changes are very minor)

My scenario assumes that from 2012 forward, NA’s consumption (solid brown line) equals its population (as projected by the US

As illustrated in Figure 24, NA’s consumption rate from 2012 and on continues along its recent upward trend as the population increases at about 1%. The good-old days have returned! In contrast, the rest of the world suffers an immediate 40% drop in consumption, but then resumes an upward trend as world population continues to increase.

The cumulative amount of petroleum produced (Q), shown as the blue line (amounts in billions of barrels according to the right axis labels), illustrates the looming problem with this fantasy scenario.

If NA’s and the rest of the world’s production is allowed to continue as assumed here, Q∞ is reached in 2036-2037 at which point production drops to zero for everyone—only 26 years from now.

Of course, the year when Q∞ is reached and production hits zero can be hastened or postponed by increasing or decreasing the rest-of-world’s assumed consumption rate: at 4 b/py, Q∞ is reached in 2028; at 1 b/py Q∞ is reached in 2047; and at 0 b/py Q∞ is reached in 2064. Petroleum production rates hitting zero would probably put the world back at a century or more in standard of living.

Additionally, this fantasy scenarios does not even consider the likely increased energy costs (i.e., decreasing ERoEI) associated with extracting the last few percentages of petroleum as we approach Q∞.

I hope that this little interlude illustrates why having the “most powerful military on the planet,” a sociopathic leader, the assumption of no detrimental ERoEI effects going to 100% ultimate recovery, and even magic factor X, still doesn’t solve the predicament that the USA is in. The USA

--------------------

In the seventh part in this series, I will discuss the correlation between petroleum production and population growth and possible future trends in population change in view of declining production.