Show me the few that stayed. Farming is corporate now; there is still the myth of the family farm. Yea, you still have some fractional percent that are still out there, but they are working at Wal-Mart to pay for it, so that they can grow 100 acres of corn. There is nobody that stays on the land. There is kind of a resurgence in it, but it's San Francisco hippies that are going to grow some strawberries, and don't realize that agriculture is 10,000 years of human experience ...it kind of throws you because they can afford to pay $15,000 per acre to grow strawberries, well, that's already suspect.

But industrial agriculture owns America—18 percent of all America farmers grow 91 percent of all that we consume....Subsistence farms, which now is seen as a dirty word, and it wasn't a dirty word at all—we lived extremely well...and never saw a $1000 a year income.... Forty-four percent of Americans either lived on farms or something that depended on farms, the local store or whatever. After World War II, they took a survey of what the soldiers were going to do after they came back, and they all said "we are going home."

DuPont had made a lot of money sell Nylon for parachutes, tires, and all this; Union Carbide had made a fortune from the same nitrates that they burned the people in Dresden are now blasted in to the soil to grow corn and sterilize the who mid-west. They realized that they had to create some consumers, and they said it openly in their prospectus. They said it openly in Roosevelt's and Truman's social planning: we have got to get these people off these farms and into production jobs so that they will earn money so that they can buy things, so that we can maintain a war level of profits; instead of building schools out where they live. This migration was about 11 years long, 22 million people moved, and, they founded the basis of the white underclass. 2010 interview of the late Joe Bageant, from Big Ideas (6:30-9:00 minutes)

[Announcer doing a commercial announcement before Gov. Santini's interview]

Richard: ...is brought to you by Soylent red and Soylent yellow, high energy vegetable concentrates, and new, delicious, Soylent green. The miracle food of high-energy plankton gathered from the oceans of the world.

Det. Thorn: It's people. Soylent Green is made out of people. They're making our food out of people. Next thing they'll be breeding us like cattle for food. You've gotta tell them. You've gotta tell them!

Here, in part three, I provide my summary and conclusions devoted to assessing the

USA’s food energy production and consumption (Part 1), and exports and global contribution (Part 2).

My Central Hypothesis

Although petroleum is vital to the modern industrial-style food production system, petroleum is not necessarily the rate limiting factor in food production. Anyone or more of water and soil depletion, climate change, urban encroachment of farm land, the migration of people from rural to urban settings and aging of farmers, could be, or become, the limiting factor before petroleum depletion does.

One goal of this series, really this whole set of post discussing food energy, is to test the hypothesis that one of these other factors has, or is becoming, rate limiting to food production, thereby causing a slow-down in food production globally, in the USA, or in other regions, as compared to the growth in the production rate in the previous decades, at least since 1961 where the FAO data base starts.

Based on the available data presented here, I have to reject this hypothesis for the USA.

There were no signs of a slow-down in the USA’s net food energy production rate (Figure 1). The year-to-year change in the food energy production rate is highly variable, even when considering 5 year averages (Figure 2). This variability at least sometimes is reflective of "bad weather" if not "climate change:" years with extended episodes of draught. It is really a shame that the FAO doesn’t report more recent data, and we are stuck with data only up to 2007, as the present draught is a real doozy.

Although there is some signs for declining growth in the rate of food production, this is not a significant trend (Figure 3). The average rate of growth in food energy production since 1961 has been about 2%/yr, which is about double the population growth rate.

The USA is a Net Positive Food Energy Exporter

Although there are no signs that the

USA’s absolute food energy production is in decline, or even reaching a plateau, there are

definite signs of a plateau in absolute food energy net exports.

This is due to a combination of a peak, and slight decline, in food exports since 1980 plus an increase in food imports over the last 20 years (Figure 11).

Expressed as a percentage of net production, net exports are substantially down from a peak of 32 percent in 1980 to 21 percent in 2007 (Figure 10).

Nevertheless, the

USA has been and remains a strong net exporter of food, having had positive food energy exports throughout 1961 to 2007.

In fact, this is one of the few bright spots in an otherwise depressing trade balance picture.

Consider, for instance, the net positive trade income the USA gained from the net export of some key food items for 2007:

Table 2: Export, Import and Net Trade Values (billions USA) for selected items in 2007 |

ITEM | Exports in Value | Imports in Value | Net Trade Value |

Cereals | 21 | 1.8 | 19 |

Oils seed | 13 | 1.5 | 11 |

Meat, Offals | 8.3 | 4.7 | 3.6 |

Edible preparations | 4.4 | 3.0 | 1.4 |

Mineral fuels (oil, distillates) | 42 | 372 | -330 |

All industries | 1,162 | 2,017 | -854 |

Although the selected food items in Table 2 brought in about $35 billion USD, this net positive trade value was dwarfed by the net negative trade of -$330 billion USD, spent on importing fossil fuels, and, the negative total trade deficit of -$854 billion USD in 2007.

The value of the net-exported food items would have to go up a lot (e.g., an order of magnitude) before their positive trade value could put a significant dent in the trade deficit from fossil fuel imports alone.

The Success of the Petroleum-Driven Green Revolution

We should acknowledge the remarkable accomplishments of

America’s petroleum-driven food industrial complex over the last half-century.

First, a country holding about 5 percent of the world's population, and yet producing about 15 percent of the world's food energy production, is an enormous feat. But, this feat is even more incredible when one considers that it is only a small fraction of that population that is actually involved in food production.

Fewer than 2 percent of Americans farm for a living today (

USDA Extension).

That would be about 6.1 million people in the

USA in 2007 or,

less than 0.1 percent of the world’s population, responsible for

15 percent of the world’s food energy production.

This is truly a remarkable accomplishment and a testament to the efficiency of the industrial, petroleum-driven food production system.

The number might even be more remarkable, if Joe Bageant is right, and 18 percent of all America farmers grow 91 percent of all the food.

Second, the USA remains an important source of food energy to the world, at one time accounting for over 1/3 of world-wide food energy exports.

Even in 2007, the USA still provided 14 percent of all global food exports (Figure 15).

In absolute food energy terms, that corresponds to about 1616 PJ, or, about 3% of the world’s total food energy production (55,972 PJ in 2007, from this

post).

Perhaps 3% seems small, but 3% of 7 billion is 210 million people that are potentially supported by this food energy.

Many developing countries throughout the world are trying to emulate America's success—that is what the Green Revolution has been all about.

So long as these developing countries have access to adequate supplies of petroleum, and some other factor is not rate limiting, then I would expect continued increases in global food energy production. If the petroleum-driven Green Revolution can continue in the developing countries, I expect that the proportion and importance of USA food exports will continue to decline, as suggested by Figure 15.

Some Concerns

1. What happens as the petroleum declines?

One major concern is that this level of food production is likely only made possible by the “energy slaves”—the petroleum, and other fossil fuels, that are used to operate the machines used in the food production industry.

I anticipate that there are some who will say, “a lack of oil is no problem; people can just go back to the farm and take the place of the fossil fuel ‘energy slaves’ to produce the same amount of food.”

Let’s set aside issues like how inept America’s present population would be to productively go “back to the farm,” (starvation is a great motivator) and, the problems with exporting food in a world without oil (no need to transport food if we are all live on the farm). Let’s also set aside the negative economic implications of declining petroleum production (as in Joe's younger days, we all work as subsistence farmers making less then $1000/yr).

Let's just do the math.

Even if only 1 barrel of petroleum per person per year (1 b/py) presently is used in the food production system in the

USA (my low-ball estimate, see

Part 9), at 308 million people in the

USA in 2007, that’s 308 million barrels per year devoted to food production.

And, if 1 b/py is equivalent to ten humans working for one year (see my previous global food energy series,

Part 1), then 308 million barrels per year would be equivalent to about

3.08 billion human energy slaves per year, devoted solely to producing the food energy generated in 2007 in the USA.

So, even if the entire

US population of 0.308 billion devoted all their time and effort to food production, they would not be able to produce the same amount of food energy produced in 2007.

Indeed, I find it very doubtful that anything close to 2007’s 7871 PJ of food energy (Figure 9) could be produced with a purely manual human-driven food production system.

I am even skeptical that it would be possible to produce 2007’s 1900 PJ of food energy devoted to just the human food energy supply.

Eventually, I expect that Americans will play out this math exercise for real.

However, for reasons presented

elsewhere, I think that might not happen for several decades,

if petroleum, and not some other factor, is rate limiting to food production, and,

if other food-strapped countries don’t coming looking to the

USA for food and petroleum.

Maybe these are big ifs.

2. The Lack of Food Resilience

A second major concern is the focus on producing huge amounts of just a few crops types for the bulk of food energy production. For instance, corn, soyabean/soyabean oil and wheat accounted for 3/4 of the total net food energy production in 2007 (Figure 5).

Perhaps this is a highly efficient way to produce food energy, and, the drive for financial profit continues to push towards ever-increasing efficiency in this direction, as illustrated by the trend to produce increasing proportions of these few food types.

For instance, if the present trend continues, then I would expect that by 2020, corn will account for 90% of the food energy of all cereal crops, with wheat a distance second at 10% (extrapolating the trends in Figure 6). Reductio ad absurdum, add another 10 years and around 2030, close to 100% of all cereal crops would be corn.

This worries me.

If disease, insects or other pests, draught or other bad weather were to hit these big three crops, then there would be serious shortfall in food energy production. Of course, I would expect that such a short fall would affect exports more than domestic consumption, so the world should worry too.

Another aspect related to the lack of resilience that worries me is that the number of people involved in food production continues to decline as the operators of the small and medium farms give up, or retire, and sell their property. Along with them goes the agricultural knowledge base of past generations of farmers.

Joe Bageant scoffed at what he called "hippy" farmers, but this group might be the early indicator of a return to subsistence farming and a preservation of that knowledge base—we'll just have to see.

One thing that I am not particularly worried about is that a sudden disruption in petroleum imports would cause the present petroleum-driven food production system to permanently fail.

As I noted above, only a fraction of per capita petroleum use goes towards the food production system, e.g., 1-2 b/py as compared to a total consumption of about 20 b/py.

This is well within the amounts of oil produced in the

USA,

Canada and

Mexico.

As I suggested

elsewhere, a disruption in oil imports would likely lead to temporary food supply disruptions but, eventually there would be fuel rationing and a preferential direction of petroleum toward food production and delivery system.

3. The Large expenditure of Feed Energy on Animal-Derived Food-Energy

A third concern, or at least observation, is that the

USA expends a tremendous amount of feed energy to produce animal-derived food energy.

By-the-way, this is why you

should not worry about a “soylent Green” scenario:

the energy cost of expending feed-energy to raise people for food makes no more sense, energetically, than expending feed-energy to raise cattle or other live stock (but, if you disagree with me, you can stock up now before the rush:

Soylent Green Crackers).

Feed energy accounted for the largest proportion of domestic food energy consumption, 34 percent in 2007 (Figure 9), corresponding to 2147 PJ of feed energy. That’s even more than the direct human food energy supply. But, this large amount of feed energy resulted in the production of animal-food energy of only 764 PJ (Figure 1). That is, about 2.8 units of feed energy for every 1 unit of animal-derived food energy produced.

This conversion ratio of feed energy to animal-derived energy apparently is lower than some traditional estimates of 5:1-10:1, but higher than a revised estimates of 1.4:1 by Fairlie (see comments by George Monbiot in

Where's the beef? Or is this the end of meat?).

Apparently, the difference in these estimates lays in Fairlie’s consideration of the fact that a significant portion of feed energy is actually in the form of food waste, agricultural waste, or food processing waste that could not directly feed humans anyways (see comments by Simon Fairlie in

Kangaroos as human food, and present day intensive animal farming).

This large energy expenditure of feed on animal food-energy production also makes more sense when you consider the relative monetary value of these food items.

Consider the 764 PJ animal-derived food energy in 2007: only 110 PJ is gross exported and 61 PJ net exported (i.e., 110 PJ minus 49 PJ of animal-derived food energy imported). But, looking at Table 2 again, we see that the net trade value of meats and offals was $3.6 USD billion, which is almost 20% of the trade value of the cereals. This is despite the fact that the total net exported animal-derived food energy of 61 PJ is only 5% of the food energy content of total net exported cereal foods, (1215 PJ, Figure 12). That is, animal-derived food exports are valued about 4 times higher than the cereal food exports.

Perhaps this is why it makes financial sense to expend 2.8 units of feed-energy to produce the 1 unit of animal-derived food energy.

4. Declining food exports and increasing imports

My fourth and final concern is that the USA’s net food exports have flattened and declined.

As explained in Part 2 (Figure 11) exported food energy has been flat and declining since about 1980 while imported food energy has continued to increase.

Consequently, the

USA's relative contribution to global net food export energy has steadily diminished (Figure 15).

This might also reflect a “success” of the petroleum-driven green revolution: increasing production of cheap food entering the export market such that it is increasingly cheaper for the

USA and other developed countries to import food instead of producing and exporting the food domestically.

This could also reflect an increase in a broader diversity of foods being imported (e.g., sugars, stimulants & alcoholic beverage, fruits; Figure 12A) that are being imported in exchange for the three major mono-crops of

US production: corn, soyabean and wheat.

Either way, flattening exports and increasing imports does not bode well for the USA trade balance or for the ability of the USA to continue importing the diversity of crops needed for health living.

The scope of this series is directed to assessing food energy (as made available in the FOA Food Balance sheets) and to not food quality. But the trend towards producing and consuming greater proportions of processed or manufactured food (Figure 8) is also not a good sign for eating healthy.

Final thoughts

Yes, Joe Bageant was right, farming in America is corporate now, and increasingly devoted to corn and soyabean production.

That's where the money is, I guess.

But

No, I don't think that this means any time soon, starving

America’s will be eating “Soylent Green.”

Still, the direction of food production, consumption and declining exports all point to an increasing fragile food system.

There are not too many comments, or page views, for this, or the past global food energy series. Maybe it’s all too obvious, or, not as sexy as peak oil. Or, maybe people don’t understand what they are looking at because they have no frame of reference from past studies. Perhaps it takes some time getting use to looking at this kind of data.

I believe that this, and the last series, provides a unique perspective on food production, consumption and exports that, at least, I have not seen elsewhere. As best I can tell, no one has every tried to take the food quantities reported in the FAO’s food balance sheets, convert these into energy equivalents, and then aggregate them to produce estimates of total net production consumption and exports, as done here.

I will push on.

------------------------------

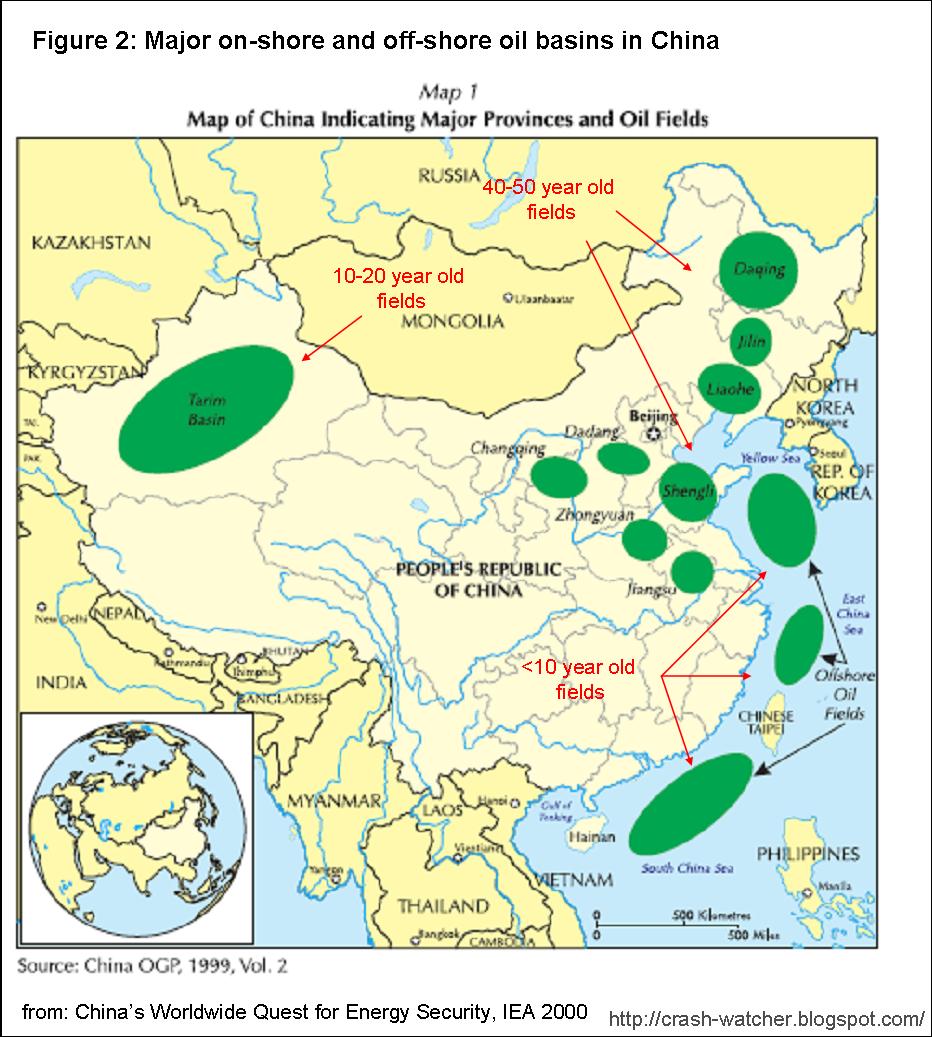

So, where to next?

How about

China?