We talked a lot about climate change today. I predict than in three or four years, we won’t be talking about climate change any more. We will be talking about energy scarcity, or, food shortages, or, declining water supplies. Not because we have dealt with climate, but because its one of a large family of pressures which are going to mount until finally, physical growth stops.

Dennis Meadows, 2010 lecture, Economics and Limits to Growth, the Population Institute (part 2/3 at ~1:15 minute)

To close out the year, I would like to review and comment on some recent blog articles, all posted within the last month, and, all touching on the same topic, but with slightly different perspectives. I ask you to seriously consider the implications of these articles with respect to the big picture risks that are bearing down on us.

First up, from Our Finite World. is Gail Tverberg’s article: Is it really possible to decouple GDP Growth from Energy Growth?

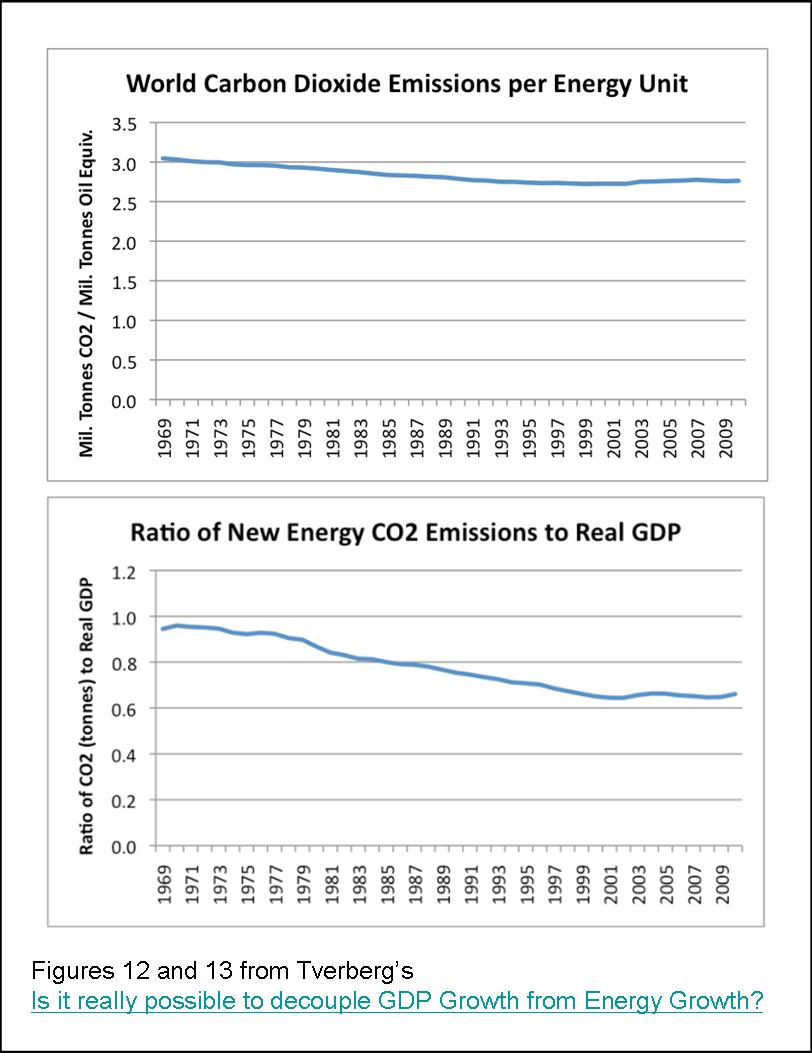

This article shows the tight relationship between total energy use and GDP for the world and various OECD countries, FSU and China. The article then goes on to depict the similarly tight relationship between CO2 emissions and energy consumption, and, between CO2 emission and GDP (the ratio ranging from about 0.9 to 0.7 for at least the last 30 years (Figures 12 and 13, respectively reproduced below):

If our intent is really to reduce CO2 emissions, it seems to me that we need to look much more broadly at the issue. Maybe the issue should be viewed in terms of (1) fossil fuel resources that we are willing to use in each future year, and (2) how much real GDP can be created from those resources, given the issues we are facing. The quantity of fossil fuels to be used each future year might consider CO2 goals as well as limits on the amount of oil that can be extracted each year because the “easy oil is gone”. The amount of real GDP that can be created from these fuels would depend on a number of factors, including declining EROI and increasing efficiency.

If the plan is to reduce fossil fuel consumption, then we may very well be expecting real GDP to also decrease, perhaps by a similar percentage. In fact, looking at the experience of FSU in Figure 9, the GDP decline may even be greater than the energy decline.

In a follow-up post, Thoughts on why energy use and CO2 emissions are rising as fast as GDP, Tverberg shows that much of the growth in CO2 emissions from the last 30 years is coming from Southeast Asia (increased oil and coal consumption) and the Middle East (increased oil and natural gas consumption), with the rest of the world being relatively flat during this period (see Figures 1 and 5 of the article).

Once again, I agree with her analysis:

The industrialization of Southeast Asia has allowed importers from around the world to reduce their energy intensity of GDP, but much of the savings has been offset by greater energy use (largely coal) in Southeast Asia . On a CO2 basis, we are likely worse off, because of this transfer.

....

The Kyoto Protocol inadvertently contributed to a pattern of greater outsourcing to Southeast Asia which was already taking place, raising worldwide CO2 emissions, while it kept emissions nearly flat (and declining relative to real GDP) in the countries doing the outsourcing.

Next up is an excellent post from Robert Rapier’s R-squared Energy Blog, at Consumer Energy Report, the article entitled, How I Would Decide the Keystone XL Pipeline Issue. Rapier’s figure showing CO2 emissions from the US

Rapier points out that CO2 emissions from the Asia Pacific are highly unlikely to decline in the near future (again with my emphasis):

My view is that regardless of what actions we take — short of going to war with China and India

....

I see mostly pie-in-the-sky from people who think we will rein in carbon emissions in China and India

Rapier’s figure reproduced above make the point clear: elevated CO2 emissions over the last 10 years are due to increased petroleum consumption in the Asia Pacific regions. This figure further illustrates that, even if North America and Europe had cut there CO2 emissions by 50% during that decade, this still would not be enough to offset all of the increased CO2 emissions from the Asia Pacific.

Referring to a funny exchange between Colbert and Bill McKibben (at 5:20 minutes), Rapier comments:

...even those who are most adamant that climate change is such a grave threat that we must take drastic measures to stop it — still rely on oil to do their business. And they really have no idea how society might respond to insufficient oil supplies — yet they are willing to take that risk for us all. But while they are aware of the threat posed by climate change, I get the impression that they are not aware of threats posed by relying on unstable regions of the world for our oil supplies.

Finally, but by no means least, are two interesting posts by David Cohen from Decline of the Empire, entitled: How To Think About The Future and For Humans, The Economy Is Everything. To fully appreciate these posts in context, you will have to first slog through his earlier post, Economic Growth And Climate Change — No Way Out?. That earlier article covers similar ground as Tverberg’s, pointing out the tight connection between fossil fuel use, GDP growth, and CO2 emissions, as nicely summed up in Cohen’s two “rules:”

(1) If the economy is growing, then anthropogenic CO2 emissions are growing

(2) If anthropogenic CO2 emissions are not growing, the economy is in recession

In How To Think About The Future, Cohen discusses a recent paper in NATURE presenting various CO2 emission scenarios by the IPCC and predicting how the consequent global warming will trigger a massive release of CO2 and CH4 from the melting arctic permafrost, viz., “the high warming scenario will degrade 9–15% of the top 3 metres of permafrost by 2040, increasing to 47–61% by 2100 and 67–79% by 2300.”

After pointing out how CO2 emissions are a good proxy for economic growth, Cohen rhetorically asks (my emphasis):

...do you find it plausible that the global economy will grow and grow for the next 39 years? If you think this is possible, or even likely, you should worry about CO2 emissions from thawing permafrost. If you don't find DAVE 1.0 plausible, and regular DOTE readers know I don't, you're likely to shrug off this Nature survey about future emissions from thawing permafrost, reasoning that there are plenty of things to worry about; this is only one of them.

For example, what will global oil production be in 2040? What will it be in 2050? In my view, it's not only likely, it's almost a certainty that global oil production will be considerably lower in 3 or 4 decades than it is right now. Perhaps you think that makes no difference to future economic growth. I beg to differ.

More pointedly, in For Humans, The Economy Is Everything, Cohen says:

Homo sapiens—yes, that's you and me folks—is not going to do diddly-squat about climate change. And why not? As if we had to learn this lesson all over again in the three years since the financial meltdown, we have once again discovered that for human beings, the economy is everything.

Stopping or slowing greenhouse gas emissions would require us to shrink the economy instead of trying to grow it. And why is that? Because modern industrial economies require lots and lots of energy to function. As the economy grows, energy consumption grows too. (Efficiency can only take you so far and according to Jevons, makes matters worse over time.) So unless we have alternative "renewable" sources of energy that scale to the levels required to support a growing global economy, we must shrink that economy to reduce emissions from burning fossil fuels. At present, and in the foreseeable future, those viable (scalable) energy alternatives do not or very likely will not exist. Got it? Do not exist.

Comment

I made the title of this post a play on the title of one of Cohen's post, because I think that his article as well as Tverberg’s and Rapier’s posts are talking about risk or relative risk. All of these posts speak to the same issue: the relative risks of the collapse of civilization due to run-away global warming versus risk of the collapse of civilization due to peak oil, and more generally peak fossil fuels, and, a realistic response to these risks.

The global warming scenarios that come out of the IPCC are all based on variants of the so-called business-as-usual (BAU) assumption: economic growth can continue on at the same rate as in the past 50 years, and thereby generate the amounts of green-house gases thought necessary to cause extreme CO2 emissions and consequent catastrophic global warming.

Underlying the BAU assumption however is a second assumption that there are enough fossil fuels, and in particular, enough of the key fossil fuel for transportation, petroleum, to sustain continued global economic growth. A third assumption is that "we," meaning the governments and people of North America and Europe, by using less fossil fuels (e.g., by driving electric cars and setting up wind turbines and solar panels) can prevent catastrophic global warming. Finally, a fourth, perhaps less explicitly stated assumption is that "we" must focus all of our efforts and resources into doing this RIGHT NOW, because it is the most important imminent risk that civilization, and all life on the planet, has ever faced.

Here then is my view of the risk scenario for catastrophic global warming and its possible mitigation.

I have several problems accepting this scenario and its mitigation:

1) There is good evidence that the world is at peak petroleum production now, and that future production will steadily decline and the fossil fuel reserves assumed to exist by the IPCC scenarios are several times overestimated (see e.g., Akelett's and Ypersele’s presentations and subsequent discussions at ASPO 9 which I previously reviewed here).

2) Petroleum is the key fossil fuel "driving" all major modes of transportation, and supporting BAU economic growth, and therefore, economic growth can no longer happen “as usual” in the face of declining petroleum production.

3) Because CO2 emissions are intimately tied, a proxy, as Cohen puts it, to economic growth, and, because the burning of fossil fuels, especially petroleum, is a prerequisite for economic growth, the levels of atmospheric CO2 are likely peaking now.

4) As Tverberg’s and Rapier's articles nicely illustrate, even if North American and European governments could get a political mandate to make an all-out effort to cut their fossil fuels consumption, the increased fossil fuel consumption in the Middle East and Asia Pacific would totally offset and likely exceed these efforts.

5) If “Cohen's rules” are correct, then North American and European governments attempting an all-out effort to rapidly decrease their fossil fuels consumption, e.g., at a greater rate than the rate of increased consumption elsewhere, such an effort would likely accelerate economic collapse in North American and Europe. And, per point (4), this would have substantially no effect on decreasing global CO2 emissions, because CO2 emissions would continue to growth in the Asia Pacific and Middle East.

In my opinion, governments, at all levels, would be better off thinking about how to mitigate a peak fossil fuel catastrophe scenario:

In addition to a collapsing economy, with all of its ensuing problems (high unemployment, loss of purchasing power due to inflation/deflation in no particular order, loss of capital and credit for investment, social unrest, war, etc...), a major concern is that the petroleum-driven food production system will experience a sharp decline as petroleum production declines. In view of continuing population growth, even a modest decline in food production rates will cause starvation, which in turn, will lead to social unrest and ultimately, war, over the remaining fossil fuel resources, in particular oil.

Under this scenario, moderate global warming may still occur, but it is an after-thought, in view of all the other immediate problems. As Dennis Meadows suggests, in a few years we will be talking about energy scarcity and food and water shortages, not climate change.

Can/will countries get ahead of this problem?

Well, I think that positive steps could be taken to mitigate the problem, although the prospects of implementing mitigation scenarios any times some don’t look very promising to me.

First, mitigation would require recognition and acceptance by governments, and the general population, that we are at or near peak oil now, and that there is no realistic energy replacement waiting in the wings—especially a replacement for the liquid transport fossil fuels.

There are signs of government and other bodies starting to at least consider the problem (see e.g., Eric Townsend’s peak oil resources page) although I am unaware of any government that has actually taken legislative action aimed at curbing the future effects of peak oil.

Second, governments could take several steps, such as suggested in The Impending World Energy Mess (e.g., fuel efficiency mandates, oil sands development, coal-to-liquids, gas-to-liquids), to mitigate the rate of decline in liquid fuels, and thereby slow the rate of economic and food production decline.

I just don’t see any of this happening soon. To the contrary, the environmental movement’s influence on politicians to make the reduction in CO2 emission in North America and Europe a first priority will likely stall a number of these mitigation efforts until there are frank fuel shortages. In the absence of mitigation, price spikes, fuel shortages and subsequent rationing will come sooner and harder.

Third, I would hope that about the same time price spikes and rationing starts, there will be a major effort underway to develop and implement a “Green Revolution 2.0” that is not so dependent on fossil fuel inputs to produce food. Local food production on multiple small farms using permaculture principles and human and animal power, is a good candidate as Green Revolution 2.0. Plus, having a much larger portion of the population being directly involved in food production would give the growing millions of unemployed people a meaningful livelihood.

However, once again, I don’t see governments doing anything to promote a “back to the farm” movement.

To the contrary, the US government appears to be intentionally shutting down smaller farming operations by swamping farmers with a myriad of regulations and requirements, and by allowing the patenting laws and enforcement run amuck in the agriculture realm. For instance, listen to this Jim Puplava interview of Kristin Canty the producer of Farmageddon, or, this G&B interview of Percy Schmeiser, the Saskatchewan farmer and seed developer who fought Monsanto—and lost. If the trend continues, by default, the only commercially produced food left to buy will be that produced by the large petroleum-driven industrial-type farming operations. This does not bode well at all for the level of preparedness of the country when declining petroleum production starts to limit food production.

In my opinion, a combination of fuel conservation, alternative liquid fuel development and a Green Revolution 2.0 could moderate the decline in food production, but probably still not enough to totally prevent starvation and death. But, perhaps it would be enough to prevent major resource wars and a rapid die-off. Perhaps, what could emerge is a sustainable no-growth civilization.

Living in a net no-growth or de-growth society, is a foreign experience to pretty well everyone alive today. How people adapt to this reality in the coming years will be a major challenge at a personal level as well as at the community and country level.

Hopefully, in 2012, we will start to see more movement in these directions, or, at least increasing recognition of impending peak oil and its risks.

---------------------------------------

Out with the old in with the new! I am happy to add Tverberg’s, Rapier’s and Cohen's to my blog role to the left.

Thanks to all of you who have visited this site over this past year, and especially those who have taken the time to leave comments. I hope that you continue to find it to be of some use.