Texas Derives its Electrical Energy from a Diversity of Sources

Before talking about EPA rules and the loss of the coal-fired power plants as an electricity source, I first will survey the longer term trend for

Texas’s electricity sources, expressed in Figure 5 as a percentage relative to the totals such as shown in Figure 3 in Part 1.

The data for Texas from 1990-2009 were taken from the EIA’s

Table 5: Electric Power Industry Generation by Primary Energy Source, 1990 Through 2010 and the 2010 data for Texas and the other states are from the EIA’s

State Electricity Profiles 2010, released January 2012

For simplicity, I lumped Natural Gas (CH4) and Other Gases (mostly propane) together. “Other Renewables” includes wind, solar (thermal & PV), geothermal sources and biogenic municipal solid waste, wood, landfill gas, etc... “Other” includes non-biogenic municipal solid waste, batteries, chemicals, hydrogen, pitch, purchased steam, sulfur, tire-derived fuels and miscellaneous technologies.

As you can see, the relative contributions from coal have gone down from 43% in 1990 to 36% in 2010, Natural Gas has also gone down from 51% in 2000 to 46% in 2010.

Nuclear (mostly in the early 1990s) and Other Renewables (mostly in the 2000s) have proportionally gone up.

A good portion of the Other Renewables likely corresponds to wind-derived electrical power, which has been a major focus of growth in

Texas in the 2000s.

For instance,

Texas passed

California in 2006 as the largest wind energy producer in the

USA (

Texas Passes California as US's Largest Wind Power Producer).

On its face,

Texas’s electricity generation looks “resilient” in that it has several different significant sources of electricity.

Some readers will sneer at my use of the word, “resilient” here, because fossil fuels and nuclear are not sustainable sources of energy.

However, hydroelectric, wind, thermal and PV solar etc... also are not sustainable in the longer term, because we need the fossil fuel or nuclear energy to build the structures and devices that are used to exploit these energy sources.

If you don’t have any oil, gas or coal, how are you going to build and position more windmills, PV panels or hydroelectric dams, or even maintain the ones that you have?

One more point about resilience.

Texas looks much more resilient than some other states, like these:

At 93%

Kentucky is almost totally dependent on coal for its electricity.

If the federal government really wants the country to transition away from coal any time soon, then

Kentucky will have to import its electricity from another state in the Eastern grid.

Maybe

Louisiana has some spare natural gas derived electricity it could sell

Kentucky?

Well, no, because

Kentucky and

Louisiana both already has a net electricity interstate trade deficit:

Kentucky since 2007 and

Louisiana since at least 2000 (from Table 10 Supply and Disposition of Electricity, for the respective states).

If natural gas prices go up, that would mean a large increase is electricity costs in

Louisiana.

And look at

Hawaii, with all that sun, wind, and geothermal natural resources: 75% petroleum and 14% coal—are you kidding me?

Hawaii is just one MENA “incident” away from rolling blackouts, or permanent blackouts if the tanker ships don’t show up anymore.

Alright, enough of the state-upmanship.

I thought that showing Figure 5-6 would give a sense of how much electricity sources can vary from state-to-state, and therefore why rules impacting one or two electricity sources (e.g., coal, and to a lesser extent gas and oil) can have a much bigger effect on some states than other states.

For instance, because

Idaho,

Washington Oregon and

California state legislatures effectively have banned new coal-fired plants, and in the case of California, prohibited utilities from entering into long-term contracts with coal-fired power plants for electricity imports, the EPA rules summarized below may not have much impact on these states. I suppose that Idaho, Oregon and Washington can afford to do this because they get 60-80% of their power from hydroelectric power sources; not surprisingly, California only get 1% of its electricity from coal.

Even though coal is not THE major electricity power source for Texas, it is a very important source, and, the losses from that source, coupled with Texas’s growing electricity use and isolated grid, is what is creating the predicament.

New EPA rules aimed at reducing air pollution

The Cross-State Air Pollution Rule (CSAPR)

Ostensibly, CSAPR was enacted to ensure state compliance with the

Clean Air Act and in particular SO

2, NOx and Ozone levels:

Mercury and Air Toxics Standards (MATS)

The EPA recently finalized the

Mercury and Air Toxics Standards (MATS), under the authority of the Clean Air Act.

MATS will cover 1,400 coal and oil-fired electric generating units (EGUs) at 600 power plants by setting national standards for all Hazardous Air Pollutants (e.g., mercury, acid gases, non-mercury metals, dioxins, SO

2) emitted by coal- and oil-fired plants with a capacity of 25 MW or more.

Incidentally, CO

2 is considered an

acid gas.

The plants covered by MATS will have 4 years to comply.

I have little doubt that MATS will also be challenged and litigated in the Courts.

Cooling water intake structures: section 316(b) rule

Under the authority of the Clean Water Act, the EPA’s

Section 316(b) Rule will enforce standards to control the location, design, construction and capacity of cooling water intake structures designed to use cooling water from various bodies of water (lake, river, etc...) to cool plants, including electric power plants and petroleum refiners.

These cooling structures must “reflect the

best technology available (BTA) for minimizing adverse environmental impact” and the goal is to reduce the mortality to fish, eggs, larvae and other aquatic organisms that come in contact with the cooling water intake (see how 316(b) could impact your power plant). Phase I rules, effecting new plants, went into effect in 2001.

The Phase II rules, to regulate existing power plants, were proposed in 2004 and suspended in 2007 pursuant to law suits filed to suspend the rule because the BTA standard was not clear, which the

Second Circuit Court of Appeals granted in part. A

final version of the Phase II rule is planned for July 2012 with the rule taking effect soon afterwards. Under the final rule, compliance with the BTA standard will likely involve the installation of cooling towers, dry cooling technology or additional intake cells to lower water velocity. Compliance with the 316(b) requirements will be concurrent with the renewal of each facility's National Pollutant Discharge Elimination System (NPDES) permit which expires every 5 years (see

how 316(b) could impact your power plant).

Coal Combustion Residuals Rule (CCRR)

The

Coal Combustion Residual Rule (CCRR) is another rule proposed by the EPA, “to regulate for the first time coal ash to address the risks from the disposal of the wastes generated by electric utilities and independent power producers.”

The EPA takes its authority to make the CCRR under the

Resource Conservation and Recovery Act (RCRA), enacted in 1976, and intended to cover the disposal of disposal of solid waste and hazardous waste.

Greenhouse Gas Regulations

The EPA has already started to regulate greenhouse gas (GHG) emissions from power plants, in the form of issuing a green-house gas permits to a natural gas-fired power plant in Texas, with ten additional Greenhouse Gas permit applications for Texas companies under review (see also U.S. Starts National CO2 Permits, Cap and Trade Works, and Other Surprises).

This follows from a December 15, 2009 EPA

finding that greenhouse gases threaten human health and welfare by causing, or contributing to, climate change.

Because GHGs are “air pollutants,” they are covered by the Clean Air Act and therefore, GHGs fall within the EPA’s jurisdiction.

As such, the EPA can broadly regulate the substances in the air we breathe.

Water vapor, carbon dioxide, methane, nitrous oxides (NOx) and ozone are all

green house gases, as are fluorocarbons, and various gaseous fluorides emitted from motor vehicles or power plants.

EPA regulation includes issuing, or not issuing, permits to power generating plants, or, setting emission standards for vehicles, based on their green house gas emission impact.

The EPA is issuing the permits in

Texas because the State of

Texas refused to do so.

Rather, a number of petitioners, including the State of

Texas, filed

petitions opposing the finding and requested a review of the finding by the Circuit Court of Appeals for the

District of Columbia.

The petitions, which included petitions from 13 other States besides

Texas, were consolidated and an

Appeal Brief filed in May 2011 requesting an oral hearing.

In December 2011 The Appeal Court denied the Petitioner’s request to stay the EPA’s regulation of GHG emissions, until the case is heard.

(See Court blocks move by oil industry to delay EPA regulation of greenhouse gas emissions). The case is scheduled to be heard in late February 2012, so we may see what happens then.

Impact of the new EPA rules on Coal-Fired Plants

Some see the Cross-State Air Pollution Rule (CSAPR, pronounced “

casper”), like the other rules summarized below, as part of a

backdoor institution of a CO2 Cap-and-trade program in the

USA, after a political implementation of this died in Congress in 2009.

For instance, the Energy Research Institute (ERI) rhetorically asks: since many air pollutant levels have gone down over the past decade anyway, why are yet more rules needed (see

Electric Grid Reliability Problems: The Result of EPA Regulations?).

The ERI’s implication is that a number of the rules directed to reducing pollution are being used to indirectly reduce CO

2 emissions.

If the EPA’s ability to implement GHG Regulations are ratified by the Courts, then this indirect approach would not be necessary. However, CSAPR, MATS, 316(b) and CCRR would be strong fall-back positions that would have essentially the same effect as direct regulation of GHGs from coal-fired power plants.

Regardless of their merits, possible hidden agendas etc..., if all of these rules go into effect it will cause some utilities operating coal-fired power plants to either install costly technology and equipment to comply with standards under the rules, or, shut down the plants where it would be too cost-prohibitive to retrofit with anti-pollution measures. I imagine that in the former case, the cost of retrofits will simply be passed on to customers, and that latter case would apply mainly to older, smaller, plants where it would take too long to recover the retrofit cost. Alternatively, utilities could just decide to reduce their use of coal-fired plants up to their annual pollution limits, and then just idle the plant thereafter.

At best, the EPA rules will give the effected States reduced costs because of less sickness and death due to cleaner air and water, but likely at the cost of higher electricity prices. At worst, the EPA rules will have little effect heath, because air pollution would go down anyways, cause increase electricity prices and cause the number of rolling blackouts to increase.

For

Texas, because of its isolated grid, I think that regardless of what else happens, there is a very good possibility of having increased days of industry load shedding and rolling black outs at least in the summer.

It depends on how many plants will shut down and whether wind can take up the slack, or not.

Estimating of Texas’s reliable electricity generating capacity

EPA Assistant Administrator Gina McCarthy has said she's confident the agency's rules won't cause electric reliability problems and will provide health benefits that far outweigh the costs. She said Thursday the Clean Air Act has mechanisms the agency has used for 40 years to protect localized reliability.

"We make sure that the lights stay on, and we achieve compliance as soon as we can," McCarthy said by telephone.

Of course, the EPA’s position is that these rules will have no effect on the reliability of electricity supplied to Texans and that

Texas has plenty of reserve electrical capacity.

However ERCOT’s Warren Lasher has pointed pointed out how the EPA has grossly over-estimated

Texas’s summer capacity, demand and reserves (CDR):

The expected maximum generating capacity in the ERCOT region in 2014 is 75,967 MW. Background documentation for the CSAPR provided by the EPA3 indicates that their projection for the operational capacity in 2014 in ERCOT is 90,405 MW, a discrepancy of 14,438 MW.

Based on an assessment of the EPA Integrated Planning Model (IPM) input database which was used by the EPA to analyze the expected impacts of the CSAPR, ERCOT believes that this discrepancy is the result of the inclusion of wind generation resources at their full name-plate capacity, and the inclusion of retired and mothballed generating capacity. ERCOT currently has approximately 9,452 MW of wind generation capacity connected to the grid. In the latest CDR, this wind generation capacity has an ELCC of 822 MW (8.7% of nameplate capacity). The discrepancy which would result from the use of the full nameplate capacity of wind versus the use of the current ELCC of wind is 8,720 MW.

Well, if the EPA is including retired and mothballed plants (corresponding to 5,784 and 2,644 MW of capacity, respectively, according to Lasher), then that’s just plain wrong on their part. But the point Lasher makes about wind deserves some further consideration.

Texas's electricity generation capacity from wind

Wind, of course, is variable and in

Texas, it blows most strongly in the fall and spring months, and, in middle of the night or early morning hours.

A wonderful example of this was presented in an article,

The Wind-Energy Myth, by Robert Bryce:

This data correspond to the first week in August 2011, when

Texas had its near-miss with rolling blackouts.

Notice the order-of magnitude different scales for total electricity demand (green) and wind-derived electricity (blue).

But what little electricity the wind did produce during these days, it was in the middle of night or early morning and not in the middle of the afternoon when demand was maximum (corresponding to the vertical dashed lines that I added).

That’s in part why Lasher comes up with an effective load carrying capability (ELCC) of only 8.7% of name plate.

In other words, even if there is 9,452 MW of wind generation capacity connected to the grid, you should only expect about 822 MW to be available at any given time.

For instance, from Bryce’s chart, on August 3, 2011 when

Texas hit its record load of 68,300 MW, at best about 1900 MW,

or about 2.7%, of that load was being provided from wind.

It turns out then, in

Revisiting Rolling Blackouts in Texas I grossly overestimated wind’s ability to provide power

at the time it was needed most as being 22% of nameplate capacity—a 2.5 times (i.e., 22/8.7) over-estimate.

Adding more wind capacity now seems to be an even less efficient solution to

Texas’s power predicament.

For instance, consider

Texas’s goal of adding add 5,000 MW power from “renewable sources,” by 2015 and of 10,000 MW, by 2025,

TEXAS RENEWABLE PORTFOLIO STANDARD SUMMARY. If this was all from wind, and it refers to nameplate capacity, then potentially only 8.7% of that capacity, or 218-435 MW by 2015, would be available when needed most in the summer afternoons. And, at a cost of

about $3.5 million per 2MW windmill (How much do wind turbines cost?), I wonder where would the $8.75 billion come from for 2500 new windmills by 2015? This sounds like pure fantasy to me.

Assessing the number plants retiring and the loss of electrical generating capacity

According to the IER, there is wide disagreement about the number of plants that will be shutdown and the amount of electricity generation capacity that will be lost due to the implementation of the first two rules, CSAPR and MATS.

The discrepancies between the EPA’s, NERC’s (North American Reliability Corporation’s) and Department of Energy’s (DOE) models for capcity loss are mainly due to their differing estimates of the numbers of plants that will be retired. The IER gets a 15,364 MW higher estimate than the EPA by including operator announcements of closures that are not counted by the EPA.

I guess that if the EPA modeling doesn’t say that a plant will close, then the EPA doesn’t count it, even if the plant says that it will close.

After reading Warren Lasher’s comments about how the EPA includes retired and mothballed plants in their estimates of

Texas’s electricity generation capacity, I can’t say that I am very confident in their country-wide estimates of retirements.

The

full IER document spells out, state-by-state, the plants that the EPA predicts will be retired and plus the additional announced retirements.

Here is the data for

Texas:

Based on these numbers, it appears that the EPA estimates a loss of 928 MW of capacity by 2015, while the IER estimates that a total of 2542 MW capacity will be lost by 2015.

For instance, the EIA doesn’t include the 1186 MW in lost capacity in 2012 due to the idling of two Monticello coal fired plants in Titus Tx, as announcement by Luminant Energy (see e.g.,

Texas power grid operator says blackouts possible).

At 1186 MW, those two

Monticello plants could generate nearly 2/3 of all the power that the entirety of

Texas’s wind-power installations were delivering (1900 MW) on August 3, 2011.

Some Rolling Blackout Scenarios for Texas

On August 3, 2011, the ERCOT region set a new peak demand record of 68,294 MW, breaking the record set in 2010 of 65,776 MW. The online capacity available for the ERCOT region on August 3, 2011 was 69,504 MW, meaning that total available generating capacity exceeded demand by only 1,210 MW, or less than 2%. Had the grid experienced forced outages of additional units, ERCOT might have had to employ rotating outages. The very next day, on August 4, 2011, in order to avert rotating outages, ERCOT had to deploy its Emergency Interruptible Load Service ("ElLS"), which is an emergency load reduction service that involves disconnecting large customers that voluntarily agree to have their service interrupted in an electric grid emergency. If another 300-500 MWs of generating capacity had been unavailable on August 4, 2011, ERCOT would have had to order rotating outages to maintain grid reliability.

That 69,504 MW capacity is lower than

Texas’s name plate capacity because, as pointed out by Lasher, at any give time, some plants are down for maintenance or repair, and, the wind isn’t always blowing.

As you can see, through contracted agreements with large industries and procuring power from Emergency Interruptible Load Services from outside of the grid, ERCOT has about 1400 MW of capacity to stave off rotating black out. This gets instituted when capacity is less than 1750 MW above demand. If capacity still exceed that 1400 MW, then when capacity is less than 350 MW (i.e., 1750-1400) above demand, rotating blackouts start.

With this information in hand, I decided to replay the summer months of 2011, but with various assumptions made about Texas’s electricity generating capacity and demand going forward.

The data set to run my scenarios is the actual daily hourly electricity demand for

Texas, as reported by ERCOT for the months of July, August and September 2011.

For example, for August 3, 2011 ERCOT provided the daily figures here:

http://www.ercot.com/content/cdr/html/20110803_actual_loads_of_weather_zones (visited August 6, 2011).

It looks like ERCOT keeps these pages for about 6 months, so eventually this data will disappear.

For instance, all data pages prior to July 1, 2012 are gone at the time of this article.

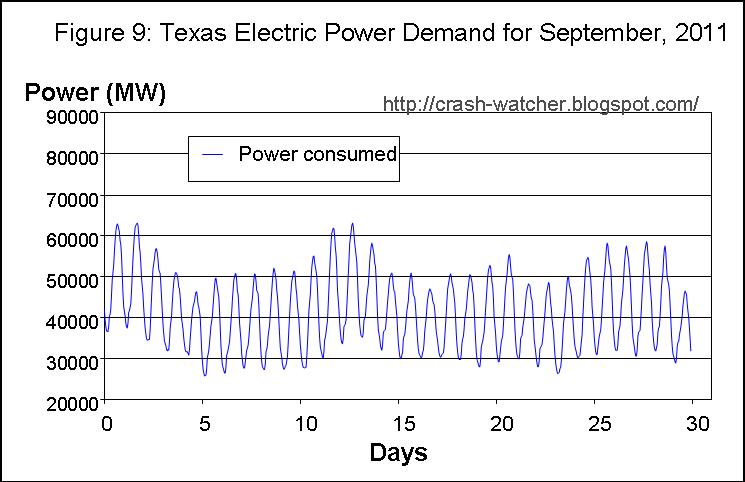

Figures 7, 8 and 9 present the ERCOT reported power demand data for the months of July August and September, respectively.

Scenario 1:

Based on Lasher’s declaration and the published ERCOT emergency levels, I will assume an electricity generation capacity throughout these three months of 69,504 MW minus the 1,186 MW in lost capacity from the two

Monticello coal-fired plants.

That might approximate the situation for 2012,

assuming no increase in demand.

Under this mild scenario ERCOT would have 68,318 MW of power capacity.

So when capacity is less than 1,750 MW above demand (i.e., Level 2, demand reaches 66,568 MW; orange line) I assume that industry load shedding and emergency services would start, and, when capacity is less than 350 MW above demand (i.e., Level 3, demand reaches 67,968 MW; red line) I assume that rotating blackout would start.

Figure 10 shows August 2011 under this scenario:

There are a total of 12 days, mostly Monday thorough Wednesday, that reach Level 2, with industry shedding and emergency services instituted and 1 day of these 12 days, August 3rd, reaches Level 3 conditions, with general rolling black out. Neither July nor September reaches a Level 2 situation.

Scenario 2:

In Scenario 2, I made the same assumptions as Scenario 1, but with the assumption that electricity demand goes up in 2012 by 2% compared to 2011.

I think that this is quite reasonable given

Texas’s previous trends for economic, population, and power consumption growth outlined in Part 1 of this series.

Figure 11 shows August 2011 under this more realistic scenario (once again neither July nor September reaches Level 2):

Under this scenario we have 17 days, over half of all the weekdays, reaching Level 2, and, 11 days of those 17 days also reaching Level 3.

Scenario 3:

In Scenario 3, I made the same assumptions as in Scenario 1, including assuming the same levels of electricity demand, except that I will assume an electricity generation capacity throughout these three months of 69,504 minus the 2,542 MW capacity that the IER estimates to be lost by 2015. That might approximate the situation by 2015, again assuming no increase in demand. Under this mild scenario, ERCOT would have 66,962 MW of power capacity. As before, when capacity is less than 1750 MW above demand (i.e., Level 2, demand reaches 65,212 MW; orange line) I assume that industry load shedding of emergency services would start and when capacity is less than 350 MW above demand (i.e., Level 3, demand reaches 66,612 MW; red line) I assume that rotating blackout would start.

Figure 12 shows August 2011 under this scenario (once again neither July nor September reaches Level 2):

Under this scenario the number of days reaching Level 2 and 3 are very similar to Scenario 2: 18 days reaching Level 2, and 11 days of the 18 days also reaching Level 3.

Scenario 4

This scenario combines Scenarios 2 and 3; I assume a 2% per year growth in power demand out to 2015 as compare to the 2011 demand (i.e., (1.02)4=1.082) and I also assumed the 2,542 MW capacity loss estimated from the IER report.

Under this more realistic scenario, there are days in all three months that reach Level 2 and 3; Figure 13-15 shows these three months under this scenario:

Things look quite grim under Scenario 4. Level 2 is reached on 21 days, 29 days and 4 days for July, August and September, respectively, for a total of 54 days out of a possible 92 days. Level 3 is reached on 17 days, 28 days, and 4 days for July, August and September, respectively, for a total of 49 days.

Only three days in August do not have at least Level 2 conditions. And, it is not just the number of days with Level 2 or 3 conditions, it is the duration of these conditions during each day. For instance, during that record day, August 3, 2011, the Level 3 condition extends from 1 pm to 9 pm. Most of the other days during August similarly have extended periods of Level 3 conditions, ranging from 1-3 pm to 6-7 pm each day.

I think that I will stop here, but keep in mind that I did not consider the possibility that the other EPA rules like, 316(b), CCR, or the GHG regulations would cause more plant closures, of that there could be more closures past 2015. These rules could be significant, however.

For instance NERC’s

2011 Long-Term Reliability Assessment (p.117-118) indicates that of the fours rules, CSAPR, MATS, CCR and 316(b), it is 316(b) that could have the biggest effect on reducing electricity reserve margins: an additional 25,000-30,000 MW nationwide, but not until 2018. NERC estimates that CSAPR and MATS could further reduce margins by another 4,000 MW and 8,000-12000, respectively, by 2018. It is not clear how much of these additional losses would apply to Texas.

Scenarios Summary

Based on the EPA estimates of closures and owner-announced plant closures, there is a good chance of rolling blackouts becoming an annual problem during the summer in Texas.

For 2012, I assumed the owner-announced shut down of 1,186 MW worth of power from two coal-fired plants in the ERCOT area of

Texas will occur.

Based on this assumption, for the month of August,

Texas should expect 12 to 17 days with Level 2 conditions leading to industrial load shedding and purchases of emergency power, and, 1 to 11 days of Level 3 conditions with rolling blackouts.

The exact number would depend on the extent to which electricity demand stays the same as in 2011 or increases by its traditional 2%.

For 2015, I assumed EPA-estimated or owner-announced shut downs of 8 coal-fired plants amounting to 2,642 MW of power will occur.

If

Texas had no increase in demand compared to 2011, I estimate 17 days with Level 2 conditions and 11 days with Level 3 conditions, again all during the month of August.

If, however, power demand goes up by 2% per year, each year till 2015, and the 8 coal-fired plants shut down, then the numbers of Level 2 and 3 days and the length of these emergency conditions during each day becomes much more wide-spread. Level 2 conditions for 54 days out of a possible 92 days, and, Level 3 conditions for 49 days, during July, August and September, and lasting for several hours each day at least during August.

Well, this has blown up into another long post, so I will save my comments and conclusions, and some additional broader analysis, for what will be the third and final installment of this series.

I hope that you will join me then.